News

3 Reasons SOUN is Risky and 1 Stock to Buy Instead

What a time it’s been for SoundHound AI. In the past six months alone, the company’s stock price has increased by a massive 264%, reaching $16.56 per share. This performance may have investors wondering how to approach the situation.

Is now the time to buy SoundHound AI, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free .

Despite the momentum, we're cautious about SoundHound AI. Here are three reasons why you should be careful with SOUN and a stock we'd rather own.

Why Is SoundHound AI Not Exciting?

Founded in 2005, SoundHound AI (NASDAQ:SOUN) develops independent voice artificial intelligence solutions that enable businesses across various industries to offer customized conversational experiences to consumers.

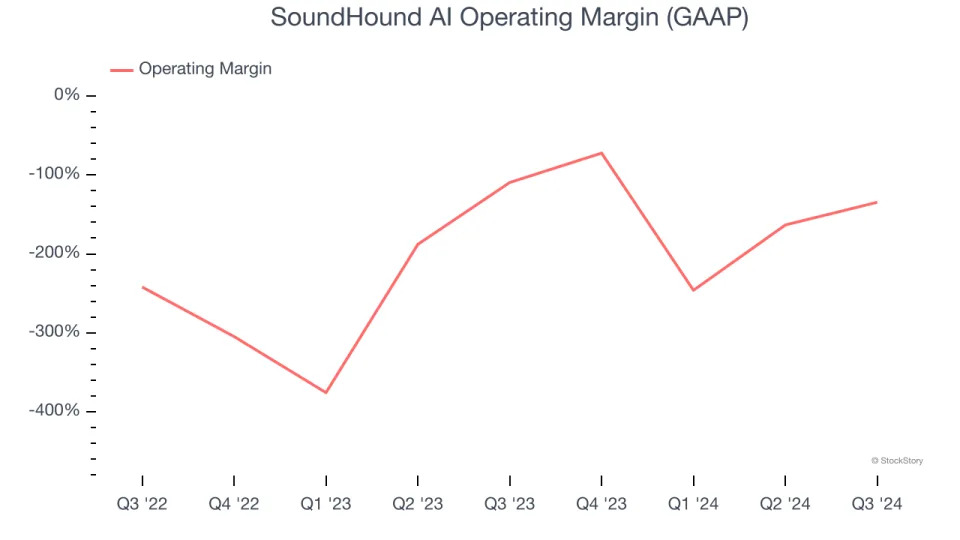

1. Operating Losses Sound the Alarms

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

SoundHound AI’s expensive cost structure has contributed to an average operating margin of negative 144% over the last year. This happened because the company spent loads of money to capture market share. As seen in its fast revenue growth, the aggressive strategy has paid off so far, and Wall Street’s estimates suggest the party will continue. We tend to agree and believe the business has a good chance of reaching profitability upon scale.

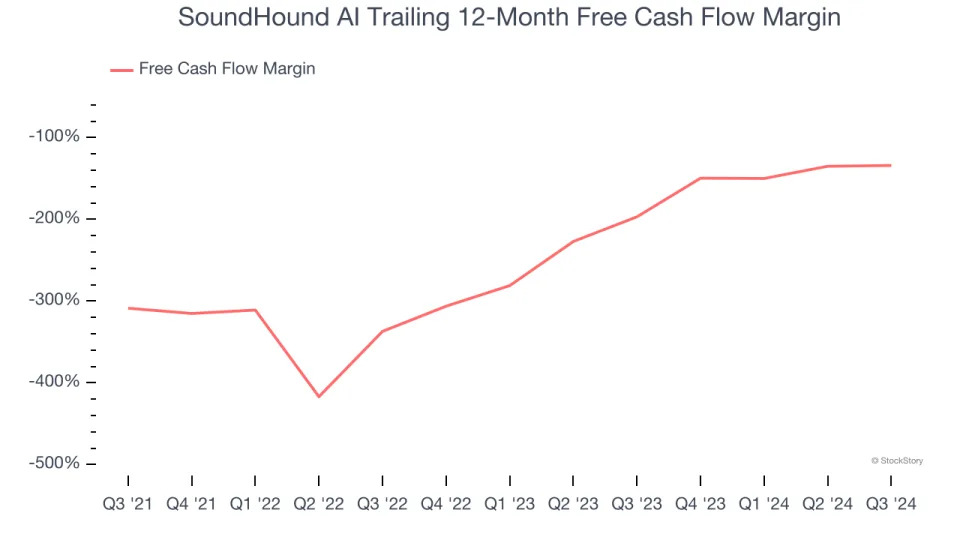

2. Cash Burn Ignites Concerns

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

SoundHound AI’s demanding reinvestments have drained its resources over the last year, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 134%, meaning it lit $134.10 of cash on fire for every $100 in revenue.

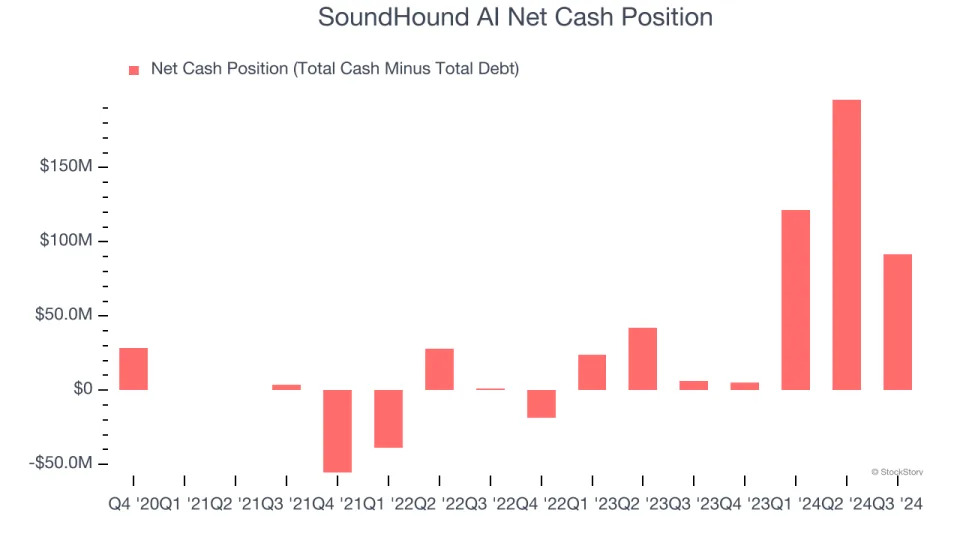

3. Short Cash Runway Exposes Shareholders to Potential Dilution

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

SoundHound AI burned through $90.24 million of cash over the last year. With $135.6 million of cash on its balance sheet, the company has around 18 months of runway left (assuming its $43.84 million of debt isn’t due right away).

Unless the SoundHound AI’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of SoundHound AI until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

Final Judgment

SoundHound AI’s business quality ultimately falls short of our standards. Following the recent surge, the stock trades at 44.8× forward price-to-sales (or $16.56 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - you can find better investment opportunities elsewhere. Let us point you toward our favorite picks and shovels play for semiconductor manufacturing .

Stocks We Like More Than SoundHound AI

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 5 Growth Stocks for this month . This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free .