News

SunOpta (NASDAQ:STKL) Posts Q4 Sales In Line With Estimates

Plant-based food and beverage company SunOpta (NASDAQ:STKL) met Wall Street’s revenue expectations in Q4 CY2024, with sales up 6.8% year on year to $193.9 million. The company’s outlook for the full year was close to analysts’ estimates with revenue guided to $790 million at the midpoint. Its non-GAAP profit of $0.06 per share was in line with analysts’ consensus estimates.

Is now the time to buy SunOpta? Find out in our full research report .

SunOpta (STKL) Q4 CY2024 Highlights:

“We delivered another solid quarter led by double-digit volume growth reflecting broad strength across our portfolio,” said Brian Kocher, Chief Executive Officer of SunOpta.

Company Overview

Committed to clean-label foods, SunOpta (NASDAQ:STKL) is a sustainability-focused food and beverage company specializing in the sourcing, processing, and packaging of organic products.

Shelf-Stable Food

As America industrialized and moved away from an agricultural economy, people faced more demands on their time. Packaged foods emerged as a solution offering convenience to the evolving American family, whether it be canned goods or snacks. Today, Americans seek brands that are high in quality, reliable, and reasonably priced. Furthermore, there's a growing emphasis on health-conscious and sustainable food options. Packaged food stocks are considered resilient investments. People always need to eat, so these companies can enjoy consistent demand as long as they stay on top of changing consumer preferences. The industry spans from multinational corporations to smaller specialized firms and is subject to food safety and labeling regulations.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

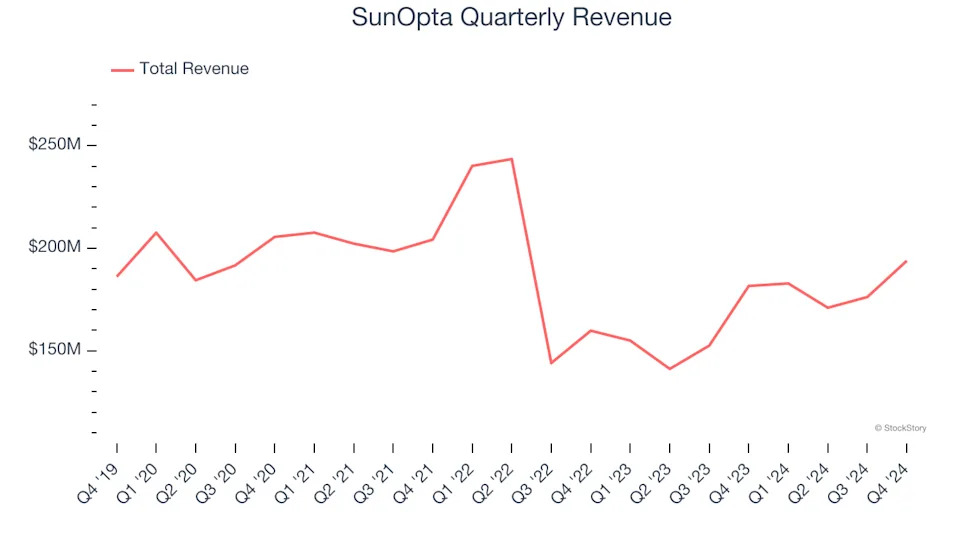

With $724 million in revenue over the past 12 months, SunOpta is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, SunOpta’s revenue declined by 3.8% per year over the last three years despite consumers buying more of its products. We’ll explore what this means in the "Volume Growth" section.

This quarter, SunOpta grew its revenue by 6.8% year on year, and its $193.9 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 8.5% over the next 12 months, an acceleration versus the last three years. This projection is admirable and suggests its newer products will fuel better top-line performance.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link .

Volume Growth

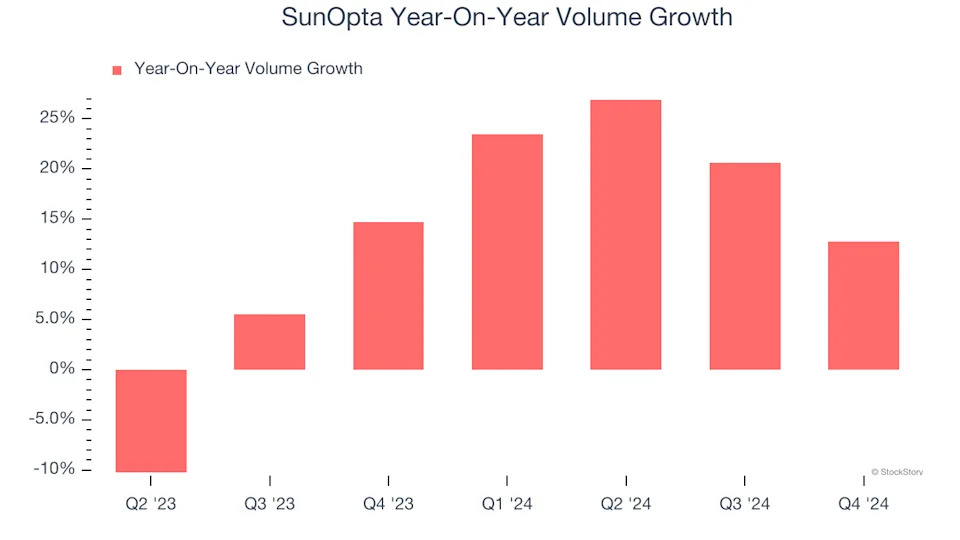

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

SunOpta’s average quarterly volume growth of 13.4% over the last two years has beaten the competition by a long shot. This is great because companies with significant volume growth are needles in a haystack in the stable consumer staples sector.

In SunOpta’s Q4 2024, sales volumes jumped 12.8% year on year. This result was in line with its historical levels.

Key Takeaways from SunOpta’s Q4 Results

It was encouraging to see SunOpta beat analysts’ EPS expectations this quarter. We were also happy its EBITDA narrowly outperformed Wall Street’s estimates. On the other hand, its gross margin missed significantly and its full-year EBITDA guidance fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 3.2% to $7.15 immediately following the results.

SunOpta may have had a tough quarter, but does that actually create an opportunity to invest right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free .