News

iHeartMedia (NASDAQ:IHRT) Misses Q4 Revenue Estimates, Stock Drops

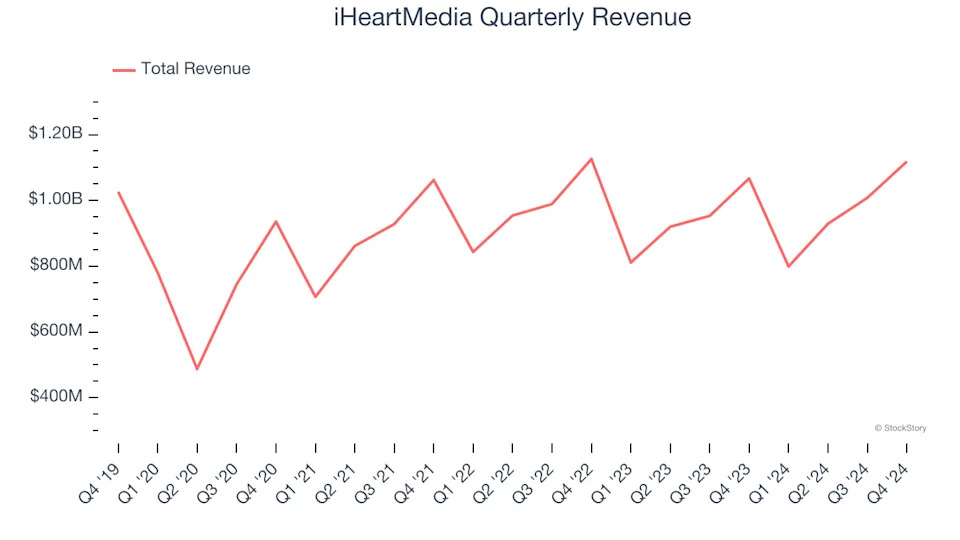

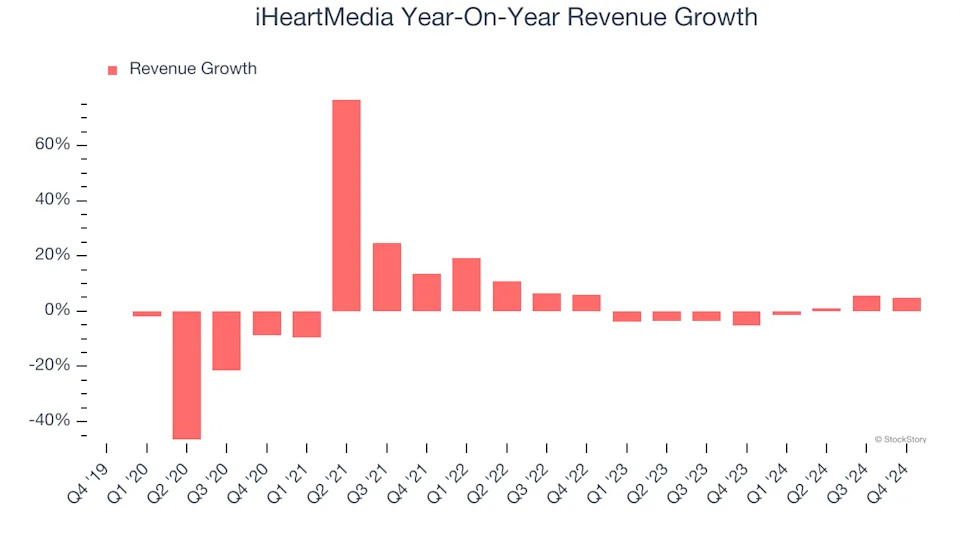

Global media and entertainment company iHeartMedia (NASDAQ:IHRT) missed Wall Street’s revenue expectations in Q4 CY2024 as sales rose 4.8% year on year to $1.12 billion. On the other hand, next quarter’s outlook exceeded expectations with revenue guided to $1.10 billion at the midpoint, or 33.7% above analysts’ estimates.

Is now the time to buy iHeartMedia? Find out in our full research report .

iHeartMedia (IHRT) Q4 CY2024 Highlights:

“Our fourth quarter Adjusted EBITDA of $246 million was up 18.2% vs. prior year, our highest percentage increase in almost three years, and our consolidated revenues were up 4.8% compared to the prior year, demonstrating the inherent operating leverage in this business,” said Bob Pittman, Chairman and CEO of iHeartMedia,

Company Overview

Occasionally featuring celebrity hosts like Ryan Seacrest on its shows, iHeartMedia (NASDAQ:IHRT) is a leading multimedia company renowned for its extensive network of radio stations, digital platforms, and live events across the globe.

Broadcasting

Broadcasting companies have been facing secular headwinds in the form of consumers abandoning traditional television and radio in favor of streaming services. As a result, many broadcasting companies have evolved by forming distribution agreements with major streaming platforms so they can get in on part of the action, but will these subscription revenues be as high quality and high margin as their legacy revenues? Only time will tell which of these broadcasters will survive the sea changes of technological advancement and fragmenting consumer attention.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, iHeartMedia struggled to consistently increase demand as its $3.85 billion of sales for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and suggests it’s a low quality business.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Just like its five-year trend, iHeartMedia’s revenue over the last two years was flat, suggesting it is in a slump.

We can dig further into the company’s revenue dynamics by analyzing its three most important segments: Multiplatform, Digital Audio, and Services, which are 61.2%, 30.3%, and 8.7% of revenue. Over the last two years, iHeartMedia’s Multiplatform revenue (broadcasting, networks, events) averaged 4.5% year-on-year declines, but its Digital Audio (podcasting) and Services (media representation) revenues averaged 6.8% and 6.7% growth.

This quarter, iHeartMedia’s revenue grew by 4.8% year on year to $1.12 billion, falling short of Wall Street’s estimates. Company management is currently guiding for a 37% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 1% over the next 12 months. Although this projection implies its newer products and services will fuel better top-line performance, it is still below average for the sector.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link .

Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

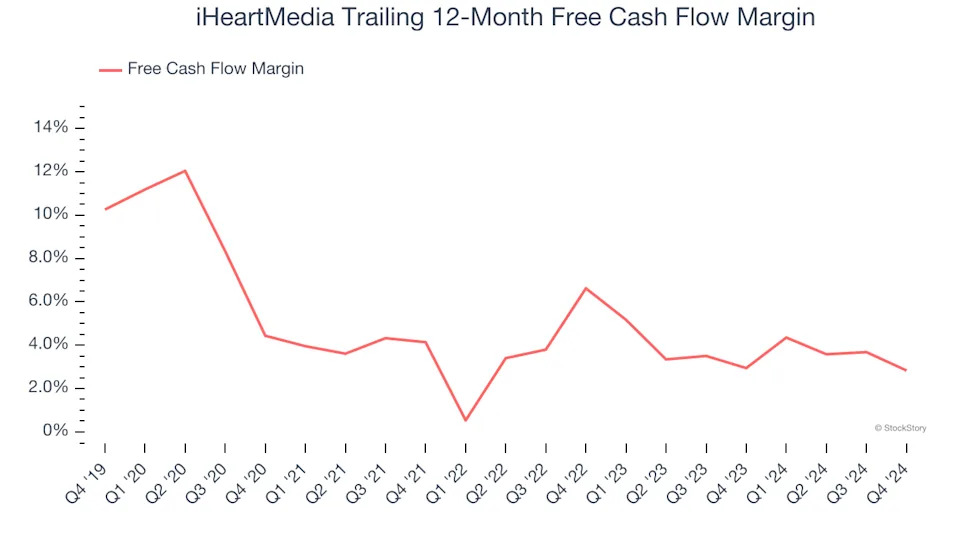

iHeartMedia has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 2.9%, lousy for a consumer discretionary business.

iHeartMedia’s free cash flow clocked in at $111.1 million in Q4, equivalent to a 9.9% margin. The company’s cash profitability regressed as it was 3.4 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, leading to short-term swings. Long-term trends trump temporary fluctuations.

Key Takeaways from iHeartMedia’s Q4 Results

We were impressed by iHeartMedia’s optimistic revenue guidance for next quarter, which blew past analysts’ expectations. We were also glad its full-year EBITDA guidance slightly exceeded Wall Street’s estimates. On the other hand, its Digital Audio revenue missed and its revenue fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 7.2% to $2 immediately after reporting.

iHeartMedia’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free .