News

Abercrombie and Fitch’s (NYSE:ANF) Q4: Beats On Revenue But Stock Drops

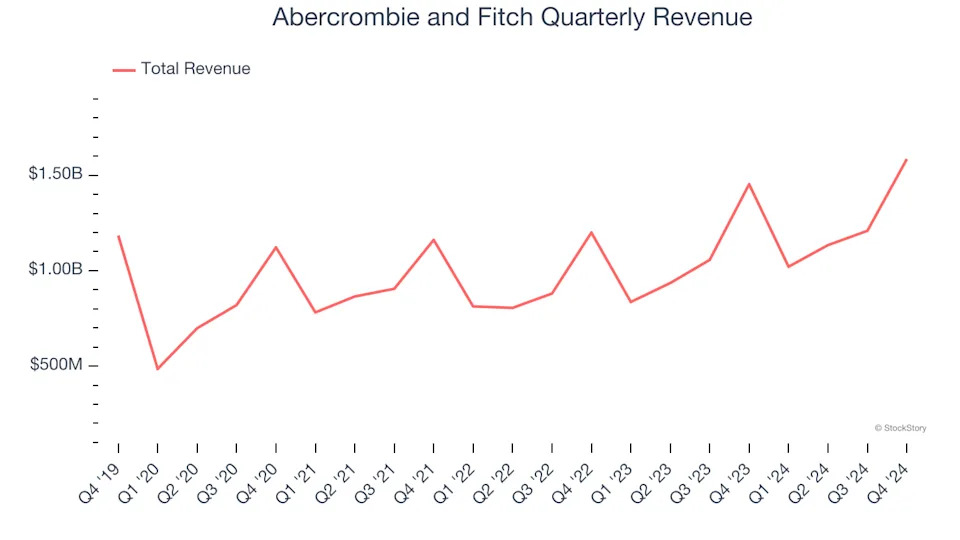

Young adult apparel retailer Abercrombie & Fitch (NYSE:ANF) beat Wall Street’s revenue expectations in Q4 CY2024, with sales up 9.1% year on year to $1.58 billion. On the other hand, next quarter’s revenue guidance of $1.07 billion was less impressive, coming in 0.7% below analysts’ estimates. Its GAAP profit of $3.57 per share was 0.8% below analysts’ consensus estimates.

Is now the time to buy Abercrombie and Fitch? Find out in our full research report .

Abercrombie and Fitch (ANF) Q4 CY2024 Highlights:

Fran Horowitz, Chief Executive Officer, said, “In fiscal 2024, we once again delivered on our commitments to our global customers and shareholders. We entered the fiscal year with the goal of achieving sustainable, profitable growth on top of a defining fiscal 2023, and our collective effort and focus produced results well beyond our initial expectations. We grew net sales 16% to nearly $5 billion while expanding operating margin to 15%, with operating income and EPS growth of 53% and 72%, respectively.

Company Overview

Founded as an outdoor and sporting brand, Abercrombie & Fitch (NYSE:ANF) evolved to become a specialty retailer that sells its own brand of fashionable clothing to young adults.

Apparel Retailer

Apparel sales are not driven so much by personal needs but by seasons, trends, and innovation, and over the last few decades, the category has shifted meaningfully online. Retailers that once only had brick-and-mortar stores are responding with omnichannel presences. The online shopping experience continues to improve and retail foot traffic in places like shopping malls continues to stall, so the evolution of clothing sellers marches on.

Sales Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years.

With $4.95 billion in revenue over the past 12 months, Abercrombie and Fitch is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

As you can see below, Abercrombie and Fitch’s 6.4% annualized revenue growth over the last five years (we compare to 2019 to normalize for COVID-19 impacts) was tepid, but to its credit, it opened new stores and increased sales at existing, established locations.

This quarter, Abercrombie and Fitch reported year-on-year revenue growth of 9.1%, and its $1.58 billion of revenue exceeded Wall Street’s estimates by 1.2%. Company management is currently guiding for a 5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 5.2% over the next 12 months, similar to its five-year rate. Despite the slowdown, this projection is admirable and suggests the market is forecasting success for its products.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link .

Store Performance

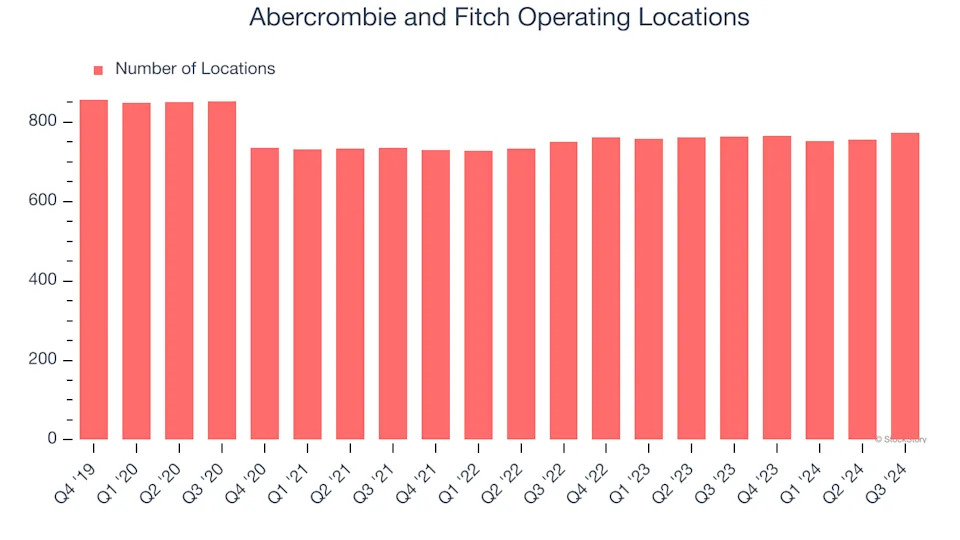

Number of Stores

Abercrombie and Fitch opened new stores quickly over the last two years, averaging 1.4% annual growth, faster than the broader consumer retail sector.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Note that Abercrombie and Fitch reports its store count intermittently, so some data points are missing in the chart below.

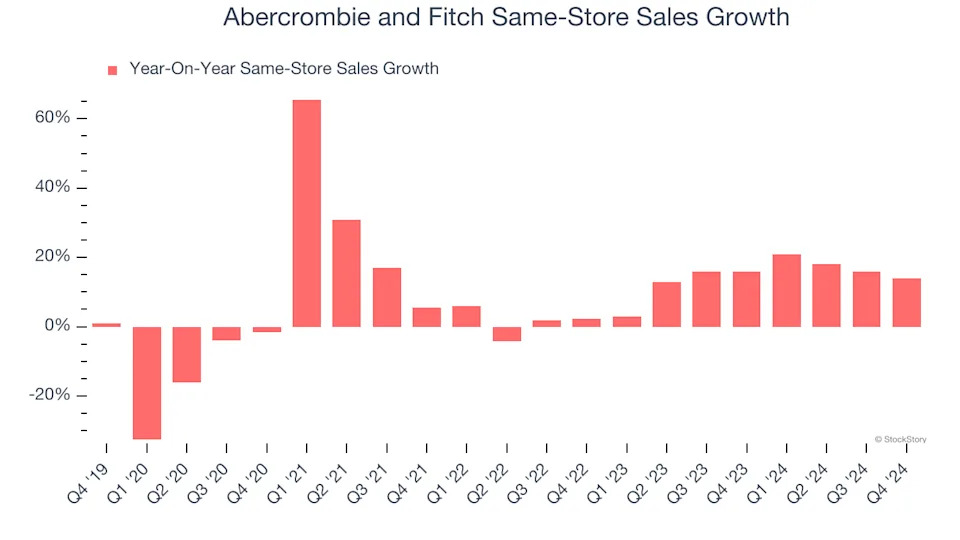

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales gives us insight into this topic because it measures organic growth for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year.

Abercrombie and Fitch has been one of the most successful retailers over the last two years thanks to skyrocketing demand within its existing locations. On average, the company has posted exceptional year-on-year same-store sales growth of 14.6%. This performance suggests its rollout of new stores is beneficial for shareholders. We like this backdrop because it gives Abercrombie and Fitch multiple ways to win: revenue growth can come from new stores, e-commerce, or increased foot traffic and higher sales per customer at existing locations.

In the latest quarter, Abercrombie and Fitch’s same-store sales rose 14% year on year. This performance was more or less in line with its historical levels.

Key Takeaways from Abercrombie and Fitch’s Q4 Results

It was good to see Abercrombie and Fitch narrowly top analysts’ revenue expectations this quarter. On the other hand, its EPS in the quarter missed and EPS guidance for next quarter missed. Overall, this quarter could have been better. The stock traded down 5.5% to $90.81 immediately after reporting.

Abercrombie and Fitch’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free .