News

3 Reasons to Sell MATW and 1 Stock to Buy Instead

Although the S&P 500 is down 1.4% over the past six months, Matthews’s stock price has fallen further to $21.21, losing shareholders 8.6% of their capital. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in Matthews, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free .

Despite the more favorable entry price, we don't have much confidence in Matthews. Here are three reasons why there are better opportunities than MATW and a stock we'd rather own.

Why Do We Think Matthews Will Underperform?

Originally a death care company, Matthews International (NASDAQ:MATW) is a diversified company offering ceremonial services, brand solutions and industrial technologies.

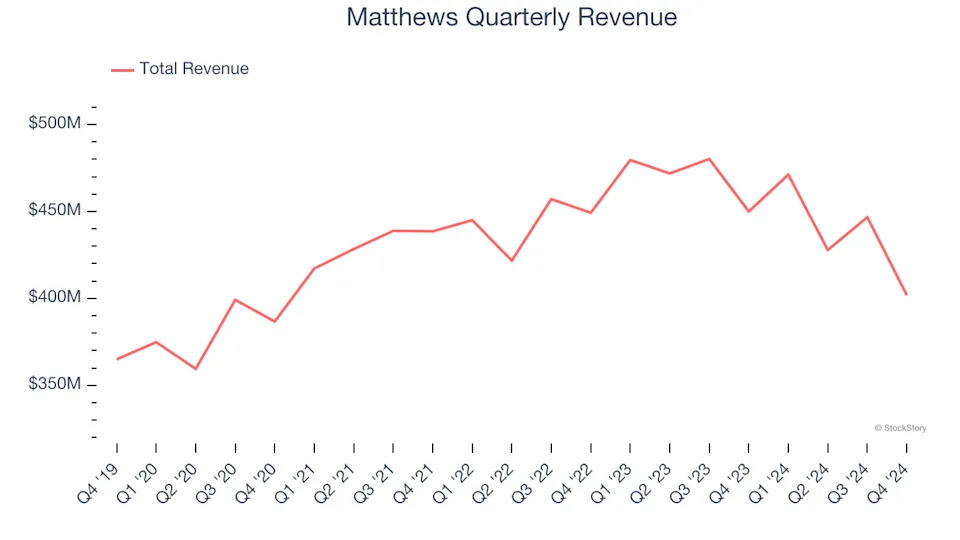

1. Long-Term Revenue Growth Disappoints

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Matthews grew its sales at a weak 2.7% compounded annual growth rate. This was below our standards.

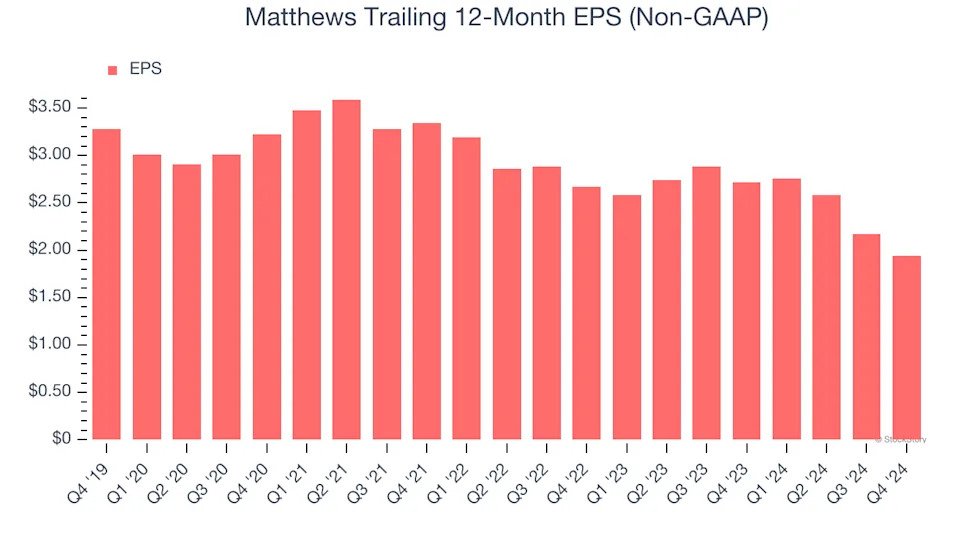

2. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Matthews, its EPS declined by 10% annually over the last five years while its revenue grew by 2.7%. This tells us the company became less profitable on a per-share basis as it expanded.

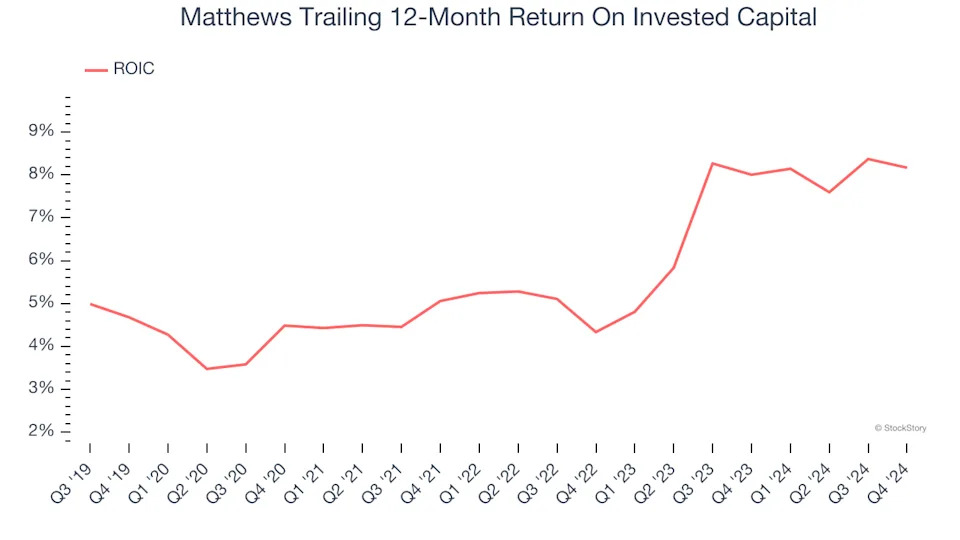

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Matthews historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 6%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

Final Judgment

Matthews doesn’t pass our quality test. Following the recent decline, the stock trades at 4.5× forward EV-to-EBITDA (or $21.21 per share). While this valuation is reasonable, we don’t see a big opportunity at the moment. There are more exciting stocks to buy at the moment. We’d recommend looking at one of our top digital advertising picks .

Stocks We Like More Than Matthews

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 5 Strong Momentum Stocks for this week . This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free .