News

3 Reasons to Sell G and 1 Stock to Buy Instead

Even during a down period for the markets, Genpact has gone against the grain, climbing to $50.06. Its shares have yielded a 27.5% return over the last six months, beating the S&P 500 by 29.2%. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy Genpact, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free .

We’re glad investors have benefited from the price increase, but we're swiping left on Genpact for now. Here are three reasons why there are better opportunities than G and a stock we'd rather own.

Why Is Genpact Not Exciting?

Originally spun off from General Electric in 2005 to provide business process services, Genpact (NYSE:G) is a global professional services firm that helps businesses transform their operations through digital technology, AI, and data analytics solutions.

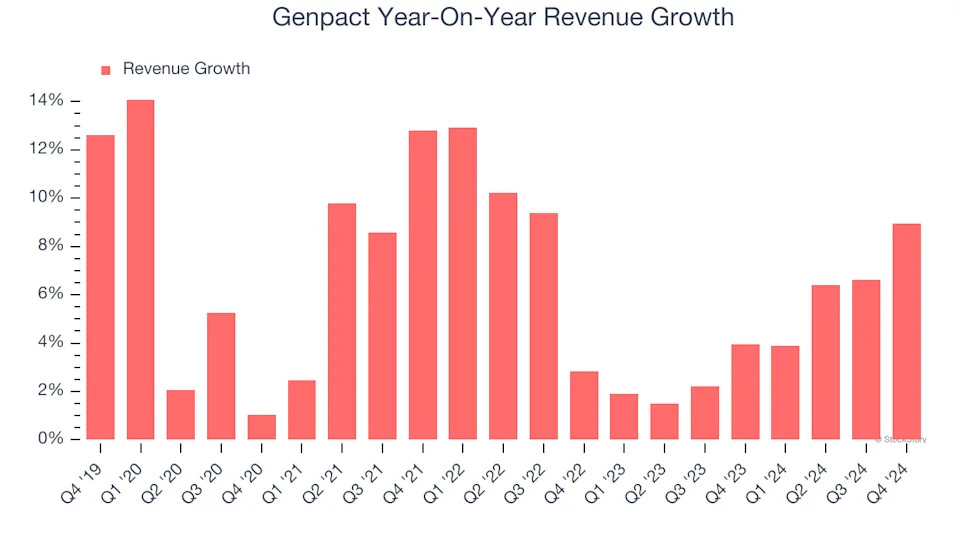

1. Lackluster Revenue Growth

We at StockStory place the most emphasis on long-term growth, but within business services, a stretched historical view may miss recent innovations or disruptive industry trends. Genpact’s recent performance shows its demand has slowed as its annualized revenue growth of 4.4% over the last two years was below its five-year trend.

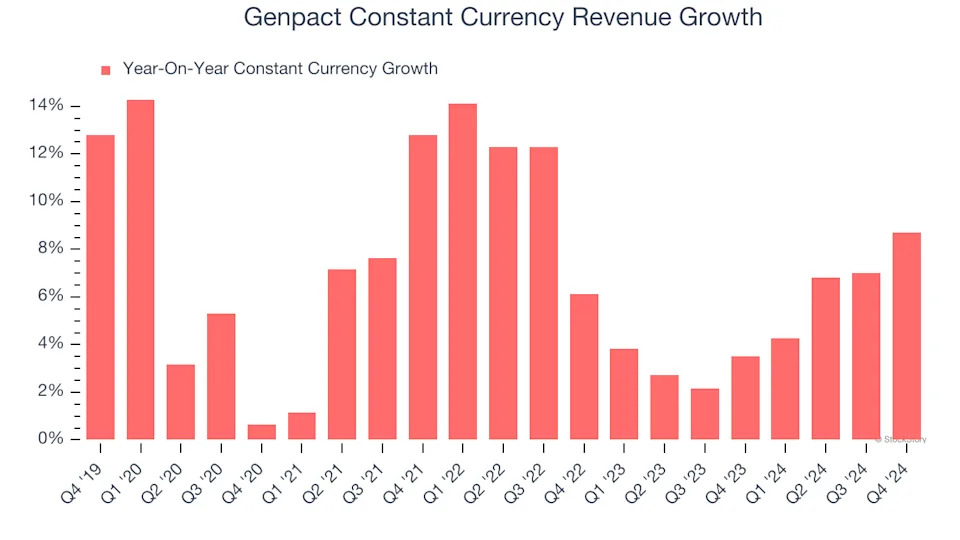

2. Weak Constant Currency Growth Points to Soft Demand

We can better understand Business Process Outsourcing & Consulting companies by analyzing their constant currency revenue. This metric excludes currency movements, which are outside of Genpact’s control and are not indicative of underlying demand.

Over the last two years, Genpact’s constant currency revenue averaged 4.9% year-on-year growth. This performance slightly lagged the sector and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

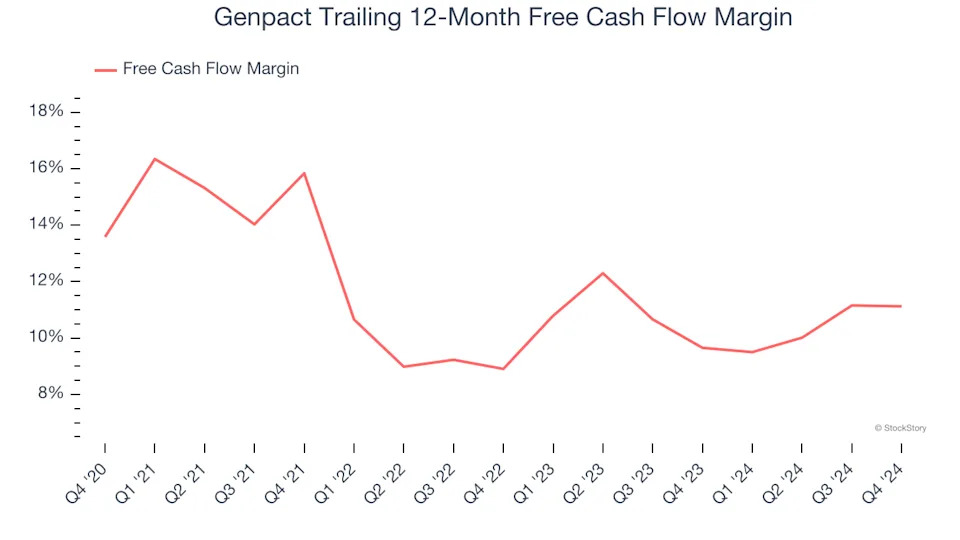

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Genpact’s margin dropped by 2.5 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Genpact’s free cash flow margin for the trailing 12 months was 11.1%.

Final Judgment

Genpact isn’t a terrible business, but it doesn’t pass our bar. With its shares topping the market in recent months, the stock trades at 14.8× forward price-to-earnings (or $50.06 per share). Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're fairly confident there are better investments elsewhere. We’d suggest looking at one of Charlie Munger’s all-time favorite businesses .

Stocks We Would Buy Instead of Genpact

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 9 Market-Beating Stocks . This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free .