News

3 Reasons to Avoid MMSI and 1 Stock to Buy Instead

Since April 2020, the S&P 500 has delivered a total return of 121%. But one standout stock has doubled the market - over the past five years, Merit Medical Systems has surged 247% to $105.49 per share. Its momentum hasn’t stopped as it’s also gained 10% in the last six months, beating the S&P by 13.3%.

Is now the time to buy Merit Medical Systems, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free .

We’re happy investors have made money, but we're sitting this one out for now. Here are three reasons why we avoid MMSI and a stock we'd rather own.

Why Is Merit Medical Systems Not Exciting?

Founded in 1987 and now offering over 1,700 patented products across global markets, Merit Medical Systems (NASDAQ:MMSI) manufactures and markets specialized medical devices used in minimally invasive procedures for cardiology, radiology, oncology, critical care, and endoscopy.

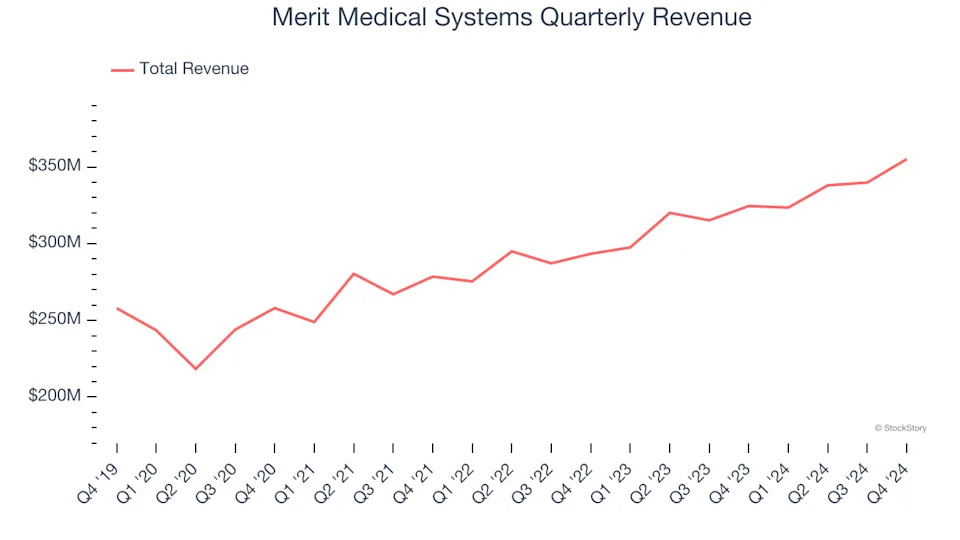

1. Long-Term Revenue Growth Disappoints

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Merit Medical Systems’s 6.4% annualized revenue growth over the last five years was mediocre. This was below our standard for the healthcare sector.

2. Fewer Distribution Channels Limit its Ceiling

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $1.36 billion in revenue over the past 12 months, Merit Medical Systems is a small company in an industry where scale matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

3. Previous Growth Initiatives Haven’t Impressed

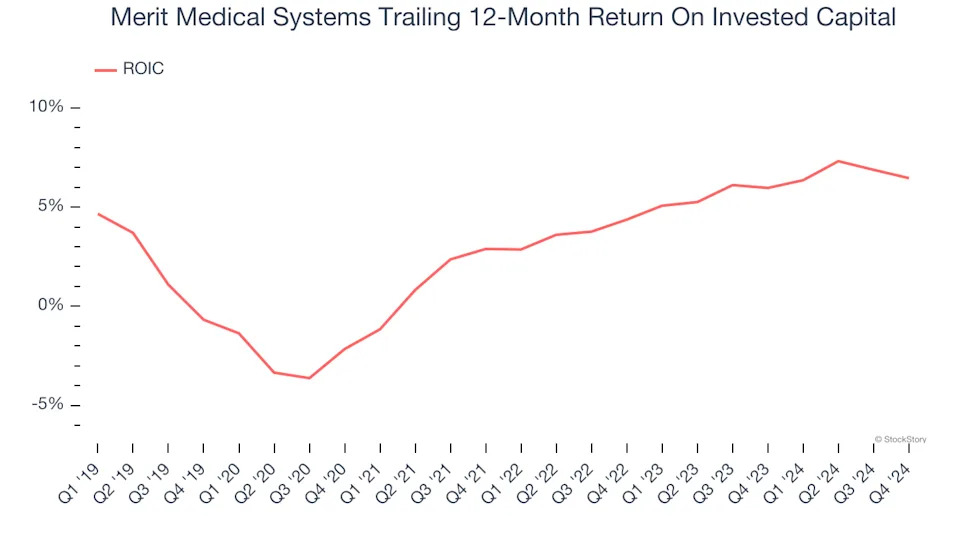

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Merit Medical Systems historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 3.5%, lower than the typical cost of capital (how much it costs to raise money) for healthcare companies.

Final Judgment

Merit Medical Systems’s business quality ultimately falls short of our standards. With its shares outperforming the market lately, the stock trades at 28.6× forward price-to-earnings (or $105.49 per share). This multiple tells us a lot of good news is priced in - you can find better investment opportunities elsewhere. We’d suggest looking at the AmazonandPayPal of Latin America .

Stocks We Like More Than Merit Medical Systems

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 5 Strong Momentum Stocks for this week . This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free .