News

Guess (NYSE:GES) Posts Better-Than-Expected Sales In Q4, Stock Jumps 10.1%

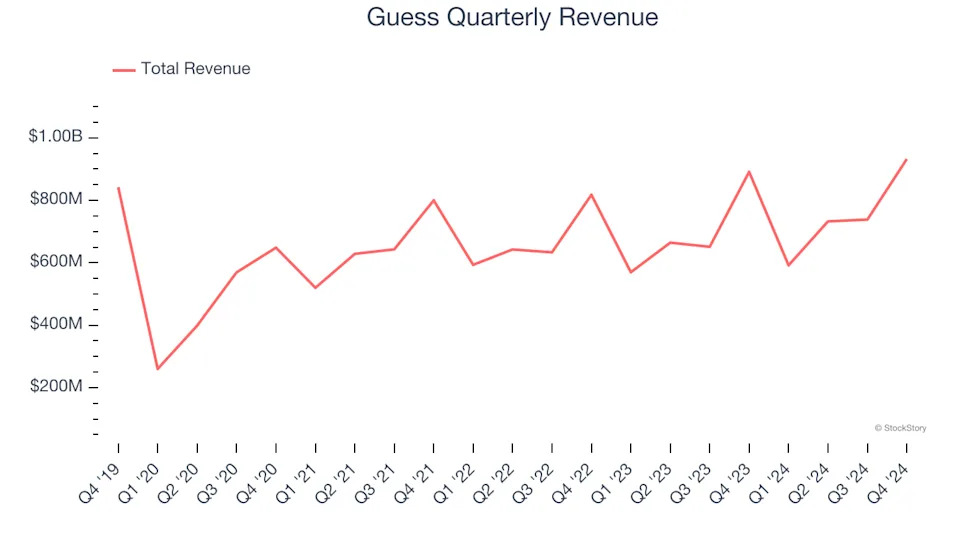

Contemporary clothing brand Guess (NYSE:GES) reported Q4 CY2024 results topping the market’s revenue expectations , with sales up 4.6% year on year to $932.3 million. Guidance for next quarter’s revenue was better than expected at $631.3 million at the midpoint, 0.8% above analysts’ estimates. Its non-GAAP profit of $1.48 per share was 7.6% above analysts’ consensus estimates.

Is now the time to buy Guess? Find out in our full research report .

Guess (GES) Q4 CY2024 Highlights:

Carlos Alberini, Chief Executive Officer, commented, “In the fourth quarter, we delivered revenue growth of 5% in U.S. dollars and 9% in constant currency. The growth in the period was primarily driven by the rag & bone acquisition coupled with positive momentum in our wholesale businesses in Europe and the Americas and increased licensing revenues. All of our operating segments posted revenue growth, except for our Asia segment. With this performance, we closed the year with revenue growth of 8% in U.S. dollars and 10% in constant currency. During the year, we delivered solid results with our Licensing segment and our wholesale businesses in Europe and the Americas, but missed our plans for our direct-to-consumer business due to slower customer traffic in North America and Asia. All considered, for the year we reached almost $3 billion in revenues and $174 million and $180 million in GAAP and adjusted operating earnings, respectively. Importantly, this year we reached a significant milestone for our Company, as we executed our first acquisition in Guess’s history, with the addition of rag & bone to our portfolio.”

Company Overview

Flexing the iconic upside-down triangle logo with a question mark, Guess (NYSE:GES) is a global fashion brand known for its trendy clothing, accessories, and denim wear.

Apparel and Accessories

Thanks to social media and the internet, not only are styles changing more frequently today than in decades past but also consumers are shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some apparel and accessories companies have made concerted efforts to adapt while those who are slower to move may fall behind.

Sales Growth

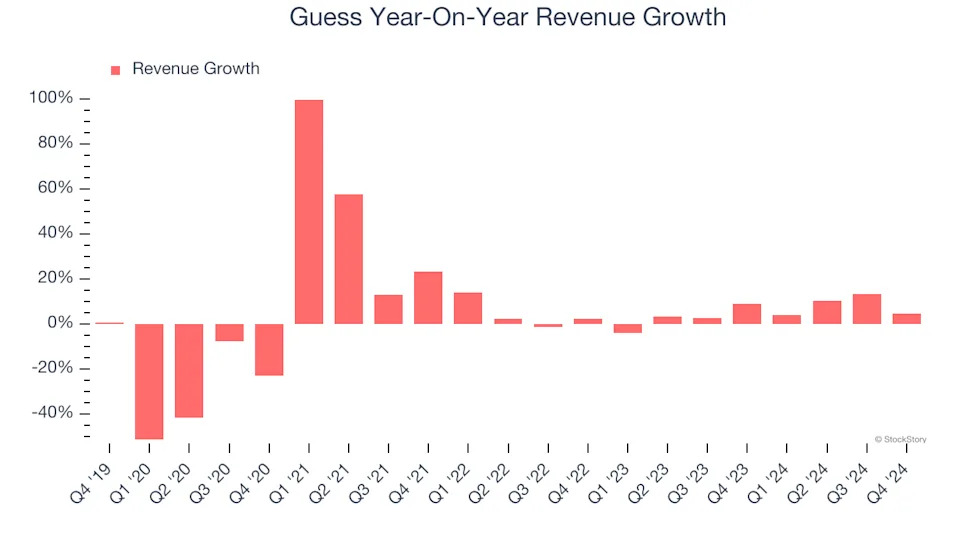

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Guess’s sales grew at a weak 2.3% compounded annual growth rate over the last five years. This was below our standards and is a rough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Guess’s annualized revenue growth of 5.6% over the last two years is above its five-year trend, but we were still disappointed by the results.

This quarter, Guess reported modest year-on-year revenue growth of 4.6% but beat Wall Street’s estimates by 2.9%. Company management is currently guiding for a 6.7% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 1% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will see some demand headwinds.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. .

Operating Margin

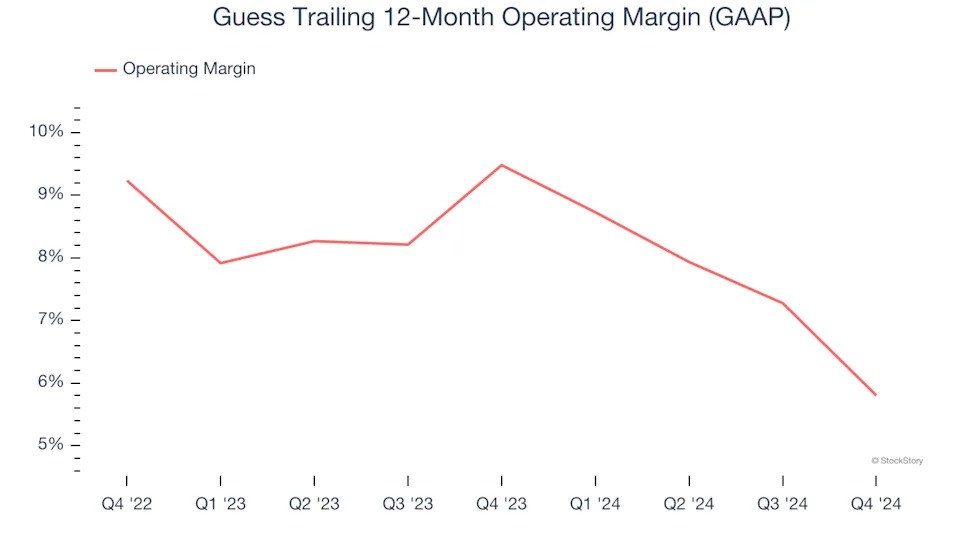

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Guess’s operating margin has shrunk over the last 12 months and averaged 7.6% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

In Q4, Guess generated an operating profit margin of 11.1%, down 5.1 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

Earnings Per Share

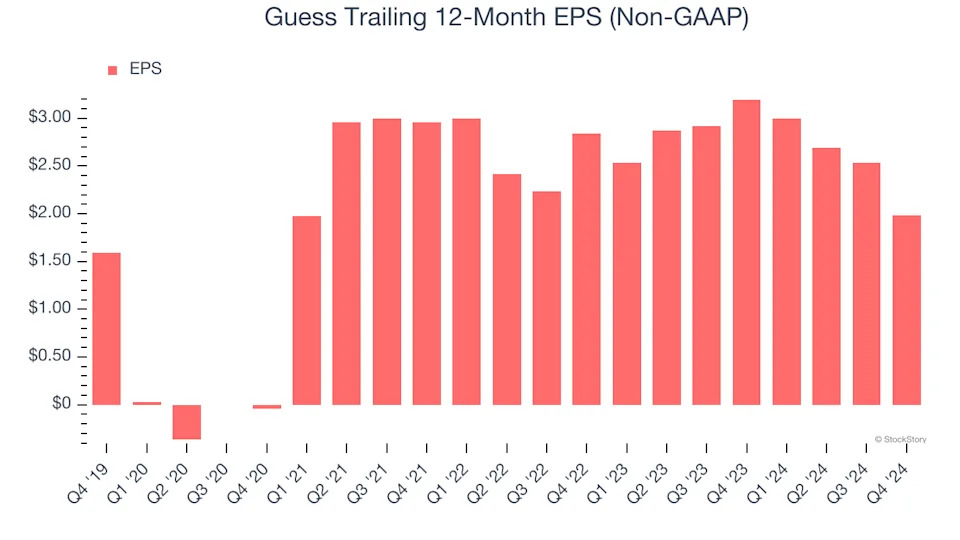

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Guess’s EPS grew at an unimpressive 4.5% compounded annual growth rate over the last five years. This performance was better than its flat revenue, but we take it with a grain of salt because its operating margin didn’t expand and it didn’t repurchase its shares, meaning the delta came from reduced interest expenses or taxes.

In Q4, Guess reported EPS at $1.48, down from $2.03 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 7.6%. Over the next 12 months, Wall Street expects Guess’s full-year EPS of $1.99 to stay about the same.

Key Takeaways from Guess’s Q4 Results

It was encouraging to see Guess beat analysts’ revenue and EPS expectations this quarter. We were also happy its revenue guidance for next quarter topped Wall Street’s estimates. On the other hand, its full-year EPS guidance missed. Overall, this was a mixed quarter. The stock traded up 10.1% to $11.10 immediately following the results.

Is Guess an attractive investment opportunity right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free .