News

PepsiCo Stock (NASDAQ:PEP) at 2021 Prices: Is It Undervalued Now?

PepsiCo stock (PEP) is currently at around the same level it was trading at in late 2021 and most of 2022 , reflecting the pressure that has weighed on Consumer Staples stocks in recent years. While some of this pressure can be attributed to higher interest rates, it’s important to note that PepsiCo has made substantial progress during this period. In fact, the company is on track to achieve record earnings per share (EPS) this year, projected to be nearly 22% higher than in 2022. Considering this strong performance and the potential for interest rate cuts later in the year, I am bullish on PEP stock and think it’s undervalued.

Why Has PepsiCo Stock Underperformed in Recent Years?

Elevated interest rates in recent years have weighed down PepsiCo’s stock price, as they have across the Consumer Staples sector, particularly for dividend-paying stocks. Rising interest rates increase the attractiveness of bonds and other fixed-income investments, often leading investors to shift away from dividend-paying stocks.

This shift in investor preference can pressure stocks like PepsiCo, which is often held in dividend-oriented portfolios due to its reliable dividend growth—having raised its dividend for 53 consecutive years. As a result, despite PepsiCo’s earnings growth during this period, its stock has been impacted as investors pursue higher yields elsewhere in search of a more favorable risk/reward balance.

Superb Earnings Growth Should Move the Needle

Despite the effect of rising rates on PepsiCo stock, the company’s superb earnings growth is poised to move the needle and translate to notable share price gains. This is particularly true given that PepsiCo is set to see its EPS jump significantly this year and because the market expects the Fed’s first interest rate cuts by year-end. Let’s examine the company’s most recent Q2 results, which have laid a strong foundation for this success.

Q2 Results: Excellent Earnings Growth Despite Slow Revenue Growth

At first glance, PepsiCo’s Q2 results might seem underwhelming, with revenues barely growing. That said, I find this development totally normal. A growth slowdown is absolutely normal after the aggressive price hikes the company implemented in recent years. In the meantime, though, operating efficiencies are driving excellent earnings growth.

In the second quarter, PepsiCo reported revenues of $22.5 billion, reflecting a soft year-over-year increase of just 0.8%. While this growth rate might seem lackluster, it’s essential to consider the context of the company’s remarkable performance over the past three years. PepsiCo capitalized on the inflationary environment during these years to drive substantial revenue gains.

After a 3% revenue decline in Q2 2020 due to supply chain disruptions, PepsiCo saw outsized increases of 20.5% in Q2 2021, 5.3% in Q2 2022, and 10.4% in Q2 2023, thanks to aggressive price hikes and strong demand for its brands. With inflation moderating over the past year and the company likely aiming to maintain product demand by avoiding further price increases, it is not surprising to see revenue growth stabilize at this point.

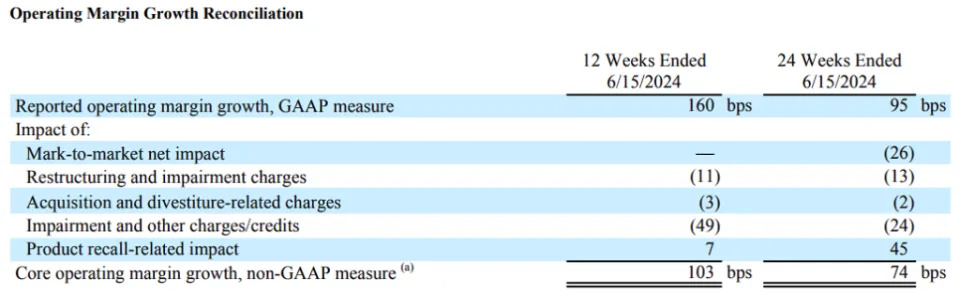

What’s important today, however, is that even with revenue growth easing, PepsiCo’s earnings growth remains exceptional. The company focused on internal improvements and cost control measures, expanding its core operating margin by 103 basis points, as you can see below.

This margin expansion and PepsiCo’s routine buybacks led to its adjusted EPS increasing by 10% to $2.28. This follows a notable 14% rise in core EPS during Q1 and, coupled with a positive outlook for the latter half of the year, sets the stage for excellent full-year growth. Management expects an increase of at least 8% in constant-currency core EPS for the year.

Given the company’s historically conservative management approach and the current momentum in earnings growth, I believe PepsiCo is well-positioned to achieve constant-currency core EPS growth of at least 10% for the year. This would translate to an estimated core EPS of around $8.27.

Valuation Seems Attractive, With Rate Cuts on the Way

As I mentioned earlier in the article, PepsiCo’s growing earnings against its relatively stagnant share price have resulted in an attractive valuation, particularly with rate cuts on the way. While shares are still trading at the same levels they did in 2022, my core EPS estimate of $8.27 implies a 22% increase from FY2022 core EPS of $6.79.

In the meantime, PepsiCo’s current stock price implies a forward P/E ratio of roughly 21x. This valuation is quite appealing for a company of PepsiCo’s high caliber, which rarely trades at a discount due to its distinctive qualities. With the market anticipating rate cuts later this year—potentially easing some of the pressure on the stock, as mentioned earlier—PepsiCo’s prospects look particularly promising.

Is PepsiCo Stock a Buy, According to Analysts?

Regarding Wall Street’s view on the stock, PepsiCo has a Moderate Buy consensus rating based on nine Buys and eight Holds assigned in the past three months. At $186.35, the average PEP stock price target suggests 7.2% upside potential.

See more PEP analyst ratings

If you’re uncertain about which analyst to follow for buying and selling PEP stock, Dara Mohsenian from Morgan Stanley (MS) is your best bet. Over the past year, Mr. Mohsenian has delivered an impressive average return of 11.45% per rating and boasts a 91% success rate. For more details, click on the image below.

The Takeaway

Although PepsiCo is trading at the same levels as it did in 2022 and late 2021, the company is poised to achieve record earnings per share, projected to be 22% higher than two years ago. Elevated interest rates have pressured consumer staple stocks like PepsiCo, but its strong earnings growth and operational efficiencies point to significant upside potential. With anticipated rate cuts and a reasonable valuation, PepsiCo appears well-positioned for share price gains, making it a compelling stock to consider buying at its current levels.

Disclosure