News

Domino's (NASDAQ:DPZ) Misses Q1 Sales Targets

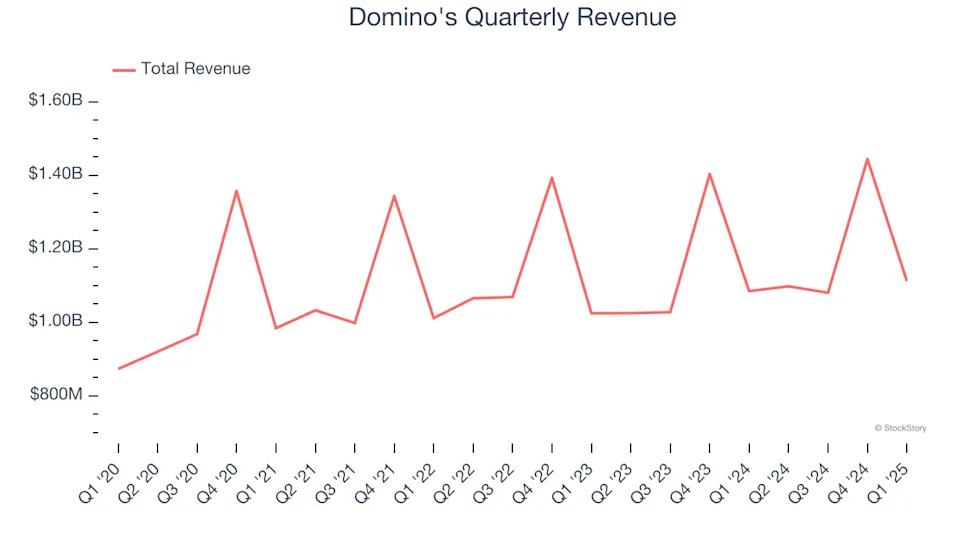

Fast-food pizza chain Domino’s (NYSE:DPZ) missed Wall Street’s revenue expectations in Q1 CY2025 as sales rose 2.5% year on year to $1.11 billion. Its GAAP profit of $4.33 per share was 6.3% above analysts’ consensus estimates.

Is now the time to buy Domino's? Find out in our full research report .

Domino's (DPZ) Q1 CY2025 Highlights:

"Domino's Q1 results demonstrate that our Hungry for MORE strategy continues to drive market share growth in QSR Pizza across both our US and international businesses," said Russell Weiner, Domino's Chief Executive Officer.

Company Overview

Founded by two brothers in Michigan, Domino’s (NYSE:DPZ) is a globally recognized pizza chain known for its creative marketing and fast delivery.

Traditional Fast Food

Traditional fast-food restaurants are renowned for their speed and convenience, boasting menus filled with familiar and budget-friendly items. Their reputations for on-the-go consumption make them favored destinations for individuals and families needing a quick meal. This class of restaurants, however, is fighting the perception that their meals are unhealthy and made with inferior ingredients, a battle that's especially relevant today given the consumers increasing focus on health and wellness.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years.

With $4.73 billion in revenue over the past 12 months, Domino's is one of the larger restaurant chains in the industry and benefits from a well-known brand that influences consumer purchasing decisions. However, its scale is a double-edged sword because there is only so much real estate to build restaurants, placing a ceiling on its growth. To accelerate system-wide sales, Domino's likely needs to optimize its pricing or lean into new chains and international expansion.

As you can see below, Domino’s 5.2% annualized revenue growth over the last six years (we compare to 2019 to normalize for COVID-19 impacts) was tepid as it barely increased sales at existing, established dining locations.

This quarter, Domino’s revenue grew by 2.5% year on year to $1.11 billion, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 6.2% over the next 12 months, similar to its six-year rate. This projection is underwhelming and suggests its newer menu offerings will not catalyze better top-line performance yet.

Today’s young investors likely haven’t read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next .

Restaurant Performance

Number of Restaurants

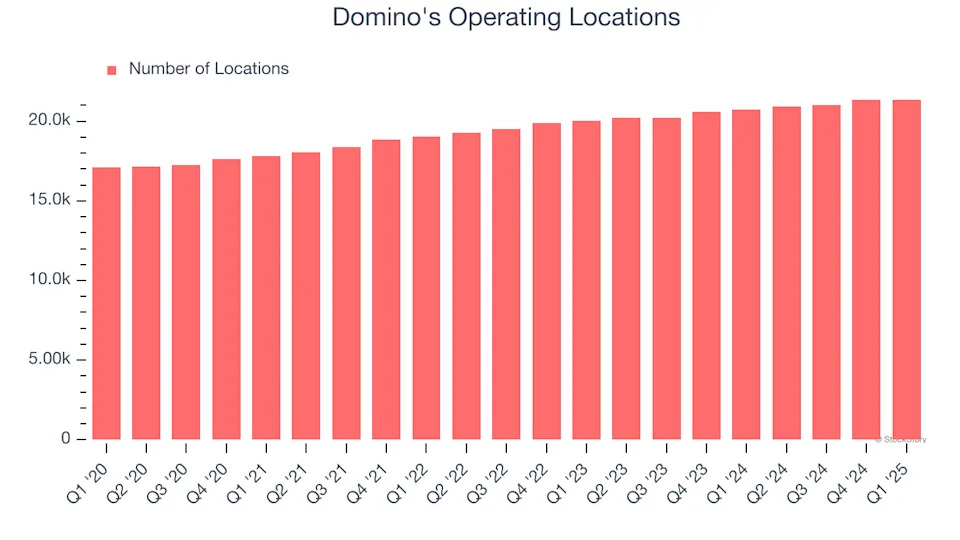

The number of dining locations a restaurant chain operates is a critical driver of how quickly company-level sales can grow.

Domino's sported 21,358 locations in the latest quarter. Over the last two years, it has opened new restaurants at a rapid clip by averaging 3.7% annual growth, among the fastest in the restaurant sector. Additionally, one dynamic making expansion more seamless is the company’s franchise model, where franchisees are primarily responsible for opening new restaurants while Domino's provides support.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

Same-Store Sales

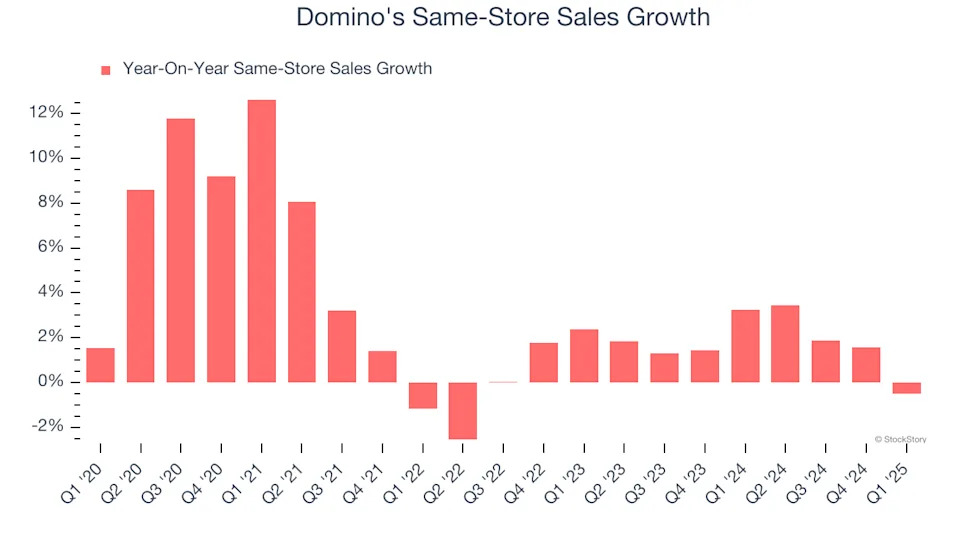

A company's restaurant base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales provides a deeper understanding of this issue because it measures organic growth at restaurants open for at least a year.

Domino’s demand within its existing dining locations has been relatively stable over the last two years but was below most restaurant chains. On average, the company’s same-store sales have grown by 1.8% per year. This performance suggests it should consider improving its foot traffic and efficiency before expanding its restaurant base.

In the latest quarter, Domino’s year on year same-store sales were flat. This was a meaningful deceleration from its historical levels. We’ll be watching closely to see if Domino's can reaccelerate growth.

Key Takeaways from Domino’s Q1 Results

It was encouraging to see Domino's beat analysts’ EPS expectations this quarter. On the other hand, its same-store sales missed and its revenue fell slightly short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 3.4% to $470.51 immediately after reporting.

Domino's didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free .