News

3 Reasons Walmart Is a Major Winner Compared to Other Retailers. Time to Buy the Stock?

Walmart (NYSE: WMT) certainly seems to be firing on all cylinders these days. Its second-quarter results were so solid, in fact, that shares reached a record high immediately following the recently released report. Moreover, based on Walmart's strong Q2 numbers, investors are deciding the economy and consumerism are healthier than presumed less than a week ago. That bodes well for rival retailers like Target and Kroger .

Just because Walmart is winning in a challenging environment, however, doesn't actually mean its competitors are as well. This company is distinctly different from other comparable store chains. Namely, it's better-positioned to thrive regardless of the economic backdrop.

But that still doesn't make the stock a buy right now.

An encouraging quarter

For the three-month stretch ending in July, Walmart turned $169.3 billion worth of revenue into earnings of $1.67 per share. That's up from year-earlier comparisons of $161.6 billion and $0.61, respectively, and better than the top line of $168.5 billion and bottom line of $0.65 per share analysts were expecting. While grocery sales drove most of the quarter's growth, same-store sales growth (U.S., excluding fuel) rolled in at 4.2%. E-commerce revenue grew to the tune of 21%, and gross margins improved too.

In other words, it was a solid quarter -- solid enough for Walmart to raise its full-year revenue and earnings guidance, and solid enough for CFO John David Rainey to comment during the second-quarter earnings call: "We have not seen any additional strain on consumer health in our business." Analysts and investors alike readily applied that observation to other retailers' businesses.

Perhaps that's a reasonably fair presumption.

It also wouldn't be unfair to presume, however, that Walmart is doing better than its rivals by taking advantage of its sheer size and subsequent capabilities. Three details from the retailer's Q2 report subtly demonstrate this superiority.

3 clues that Walmart is doing better than its competition

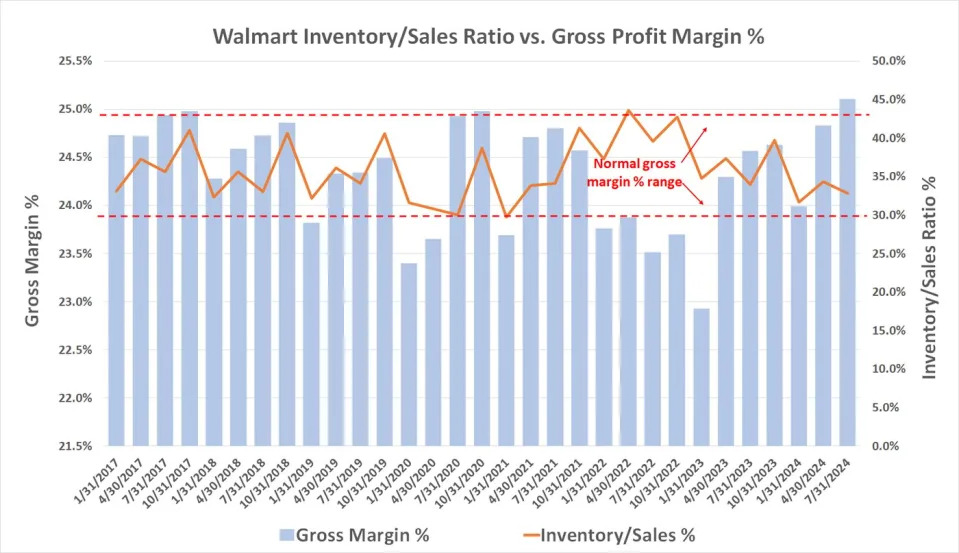

First, Walmart's inventory levels continue to fall, reaching levels not seen since before the COVID-19 pandemic took hold. As of the end of last month, the company's inventory-to-sales ratio was 32.8%, down from 2022's peak of 42.7%.

On the surface, it seems problematic -- you can't sell merchandise you don't have. But that's not the big risk in retailing. The real risk is loading up on more goods than you can sell, leaving less room (and money) for more marketable merchandise. Also, the longer inventory sits on a store's shelves, the more likely it is to get stolen, damaged, or lost.

As the graphic below shows, Walmart -- like most other retailers -- loaded up on inventory in the pandemic's latter days in anticipation of a surge in post-pandemic spending that just never materialized. Gross profit margin rates unsurprisingly tumbled shortly thereafter. As inventory levels have peeled back to more historic levels, gross margins are back to normal as well.

It's a sign that Walmart once again has a grip on how much merchandise it needs at any given time, and which merchandise it needs at any given time. Although they're certainly trying, it remains to be seen if its competition is capable of following suit.

Second, although investors don't know the specifics, Walmart disclosed that its worldwide advertising business' revenue improved 26% year over year last quarter, with this business growing 30% in the United States alone.

If you're not aware, the world's biggest brick-and-mortar store chain doesn't just make money by selling merchandise online and offline. Its shopping website also allows brands and third-party sellers to pay to promote their goods at Walmart.com. The company doesn't regularly offer much in the way of details about this operation, other than to provide a relative growth figure. Walmart did divulge in early 2022, however, that it did $2.1 billion worth of digital advertising business during the previous year. This business has grown at a pace comparable to last quarter's every year since then.

It's obviously still not a key source of revenue. This is high-margin revenue, though, leveraging an online-shopping platform Walmart would be operating whether or not it was monetized with ads. For perspective, although the retailer did $169 billion worth of business last quarter, operating income was only $7.9 billion. Its advertising arm's effect on the bottom line isn't insignificant.

It matters simply because Walmart.com is a major e-commerce destination, second only to Amazon within the United States. No other competitor is even going to come close to matching Walmart's online shopping draw. It's just too big, and too present.

Finally, although the company also continues to be coy about the specifics, Walmart+ memberships grew by double digits (again) last quarter, producing 23% growth in membership income.

The benefit of a growing Walmart+ customer base isn't readily evident. But it's there if you dig deeper. With this crowd taking advantage of their free shipping and delivery offer, last quarter's U.S. store total transaction count improved 3.6% year over year. E-commerce's growth was also led by store-based fulfillment and delivery, which in some cases can be completed the same day the order is placed.

Again, it's business-building success that other brick-and-mortar rivals will struggle to replicate simply because they don't enjoy Walmart's reach or the depth of its inventory.

To buy, or not to buy?

So the company's superior competitive position makes the stock a buy? Don't be too quick to make that move.

See, although investors should expect to pay a premium for quality picks, this high-quality name has arguably raced out of reach following the release of its second-quarter numbers. Walmart shares are currently priced at more than 27 times next year's expected earnings. Even if that consensus estimate understates what's actually in store, this stock's still uncomfortably expensive compared to its historic norm.

Just don't be too stingy or wait too long to step in. A slight cooling of the post-earnings surge may be all the pullback that's in store here. It's becoming clearer and clearer that the new-and-improved Walmart is built to thrive in any and all economic environments. Investors aren't likely to let this ticker fall much before starting to buy it again. It's just that promising a stock.

Before you buy stock in Walmart, consider this: