News

Benchmark diesel price drops a little; oil futures markets drop a lot

Oil markets are in the middle of a major downward rout, and the weekly retail diesel benchmark price used for most fuel surcharges is having trouble keeping up with the sell-off in the futures market.

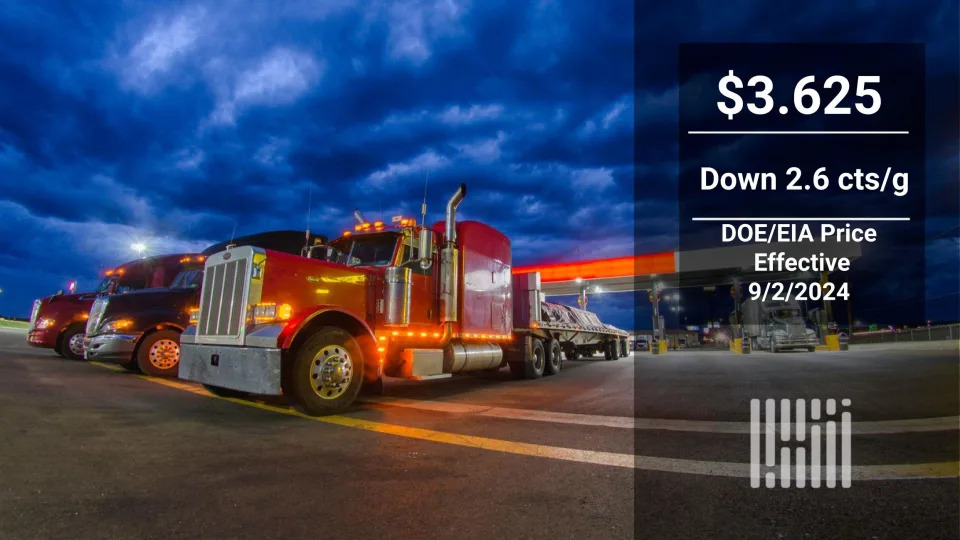

The Department of Energy/Energy Information Administration average retail diesel price fell 2.6 cents a gallon to $3.625 in a price posted Tuesday, a day later than usual due to the Labor Day holiday. (However, the effective date on the price is listed as Sept. 2.)

Retail diesel prices are always a lagging indicator. But in the minute-by-minute trading in commodity markets, the fall in all petroleum prices has accelerated, with Tuesday’s declines putting price settlements at levels not seen for many months, or years.

Ultra low sulfur diesel on the CME commodity exchange settled Tuesday at $2.206 a gallon, a drop of 4.55 cents per gallon or 2.02%. That price is for ULSD delivered in New York Harbor in October. It was the lowest settlement in the ULSD contract since Dec. 20, 2021, a span of more than 32 months.

Friday’s ULSD settlement of $2.2515 was for barrels delivered in September, but the September contract expired at the close of trading last week. The October contract became the first-month contract traded Tuesday, making the one-day decline look even more precipitous.

October ULSD settled Friday at $2.2783 a gallon, when it was the second month traded. So while a comparison of front-month Friday settlement to front-month Tuesday settle looks like the price dropped 2.2%, the reality is that is a comparison of September barrels (Friday) to October barrels (Tuesday).

Viewing the market just on the basis of comparing October to October between Friday and Tuesday results in a decline of 3.17%.

West Texas Intermediate crude oil, the U.S. benchmark, declined $3.21 a barrel Tuesday to $70.34, a drop of 3.21%. It’s the lowest settlement for WTI since Dec. 13.

Oil markets are beginning to focus on the fact that the OPEC+ group, which consists of OPEC and a group of other oil-exporting nations led by Russia, are planning on going ahead with an 180,000-barrel-per-day increase in production next month. A Reuters report , citing six sources from OPEC, created much of the market buzz Monday (when European and Asian markets were open) and into Tuesday that sent prices skidding.

“A slowdown in demand growth, notably in China, has weighed on oil prices and prompted some analysts to doubt whether the Organization of the Petroleum Exporting Countries and allies, known as OPEC+, will go ahead with the October increase,” Reuters said in its report. But the news agency said its sources had affirmed the group’s intention to proceed with the increase.

Since December, the OPEC+ group has slashed more than 500,000 barrels per day of output, according to S&P Global Commodity Insights. The pledged cuts of the group totaled 2.2 million barrels per day, implemented in stages over the past 18 months.

Virtually all of the reductions in #oil output put through by the OPEC+ group in May and June were reversed in July, per @SPGCIOil . Oh, and U.S. output was a record last week. Where would the price be if international tensions weren't propping it up? pic.twitter.com/ekw1MEHnFs

— John Kingston (@JohnHKingston) August 9, 2024

In an interview last week on Bloomberg TV, Daan Struyven, the head of oil research at Goldman Sachs, said OPEC+ has “really been quite effective at balancing the market” during the past two years, given the increases coming out of the U.S. shale patch and other countries like Guyana.

“If OPEC goes ahead with raising production, we may potentially shift to a new equilibrium with somewhat more volatility, where the new flood under oil prices becomes the breakeven price of the U.S. producer,” Struyven said.

Getting there will require lower prices, he said. “To engineer a given slowdown in U.S. shale growth, you arguably need a bigger drop in prices, because those U.S. public producers, their production plans, they’re fairly, fairly sticky, and they have very strong balance sheets,” Struyven said.

More articles by John Kingston

Parts retailer FleetPride gets lower outlook from Moody’s, but rating holds

Lender BMO’s Q3 numbers show even more trucking credit deterioration

End of an era: California Trucking Association dropping appeal against AB5

The post Benchmark diesel price drops a little; oil futures markets drop a lot appeared first on FreightWaves .