News

India credit and charge card payments market to grow by 15.5% in 2024, forecasts GlobalData

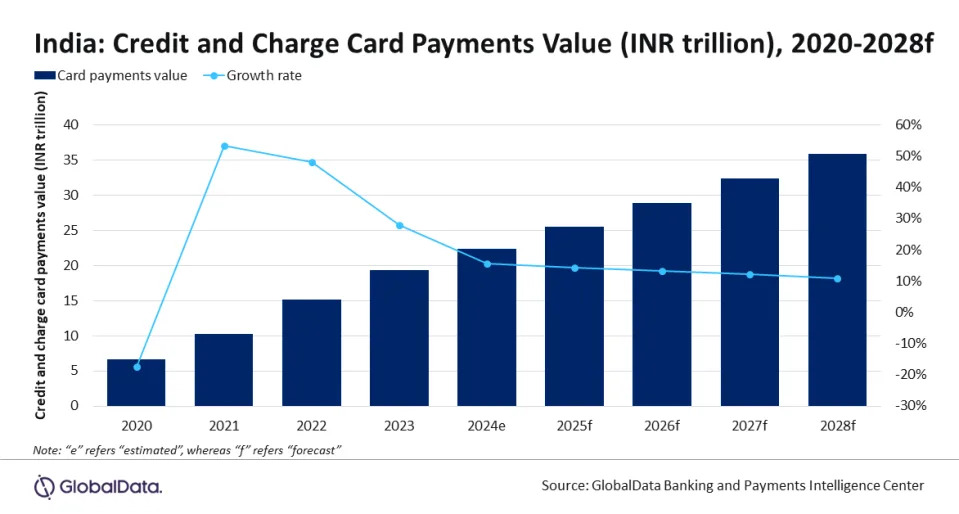

The Indian credit and charge card payments market is forecast to grow by 15.5% in 2024 to reach INR22.3trn ($270.4bn), supported by growing consumer preference for non-cash payments, according to GlobalData, publishers of RBI.

GlobalData’s Payment Cards Analytics reveals that credit and charge card payment value in India registered a growth of 48.1% in 2022, driven by a rise in consumer spending. The market continued to be on a growth trajectory, registering a growth of 27.8% in 2023 to reach INR19.3trn ($234.1bn).

Ravi Sharma, Lead Banking and Payments Analyst at GlobalData, said: “While cash dominated the consumer payments landscape in India for many decades, its use has gradually diminished in the past few years, with credit and charge cards being one of the beneficiaries. The government's initiatives, along with the increasing consumer confidence in electronic payments, have paved the way for the growth of credit and charge card payments in the country.”

Among card types, credit and charge cards are most preferred, accounting for 75.7% of the total card payment value in 2023. Payment frequency for these cards stood at 35.9 times a year in 2023 – much higher than for debit cards. Credit and charge card payment frequency is set to reach 37.6 transactions per card in 2028. This can be attributed to benefits such as reward points, discounts, and instalment payment facilities associated with these cards.

GlobalData 2023 Financial Services Consumer Survey

The rise in e-commerce payments also contributed to this growth, as credit and charge cards are widely preferred payment tools for online purchases. They accounted for 15.4% of the total e-commerce transaction value in 2023, according to GlobalData’s 2023 Financial Services Consumer Survey.

Sharma added: “Availability of flexible payment options is also contributing to the rise in usage of credit cards. Indian consumers are increasingly opting for instalment payments, with almost all major banks in the country offering credit card holders the option to convert large-ticket purchases into monthly installments.”

The government is also taking a key role in promoting card usage and improving payment infrastructure. As part of the government’s initiative to push electronic payments in the country, in January 2021, the central bank set up the Payments Infrastructure Development Fund (PIDF) to deploy one million POS devices and increase the number of merchants accepting QR code payments.

As part of this initiative, merchants in tier 3–6 cities receive subsidy on the cost of POS terminals and QR code acceptance. As of November 2023, 827,901 POS terminals and 27.2 million QR code acceptance points had been deployed using funds from this scheme, according to RBI. This initiative has now been extended to 31 December 2025.

Sharma concluded: “The future growth for the total credit and charge card payments market in India looks promising, supported by improving retail borrower behaviour and rising consumer disposable incomes. Improvements in payment infrastructure and the growth of e-commerce are also expected to support the market. Overall, the credit and charge card payments value is expected to register a strong compound annual growth rate (CAGR) of 12.6% between 2024 and 2028.”

"India credit and charge card payments market to grow by 15.5% in 2024, forecasts GlobalData" was originally created and published by Electronic Payments International , a GlobalData owned brand.

The information on this site has been included in good faith for general informational purposes only. It is not intended to amount to advice on which you should rely, and we give no representation, warranty or guarantee, whether express or implied as to its accuracy or completeness. You must obtain professional or specialist advice before taking, or refraining from, any action on the basis of the content on our site.