News

Boeing Withdraws Offer To Strikers; S&P Global Warns of Debt Downgrade

Key Takeaways

Boeing ( BA ) shares fell Wednesday after the plane maker withdrew its contract offer for its striking machinists and S&P Global put its bond rating on a watch list.

In a note to employees, Stephanie Pope—who serves as both Boeing COO and Boeing Commercial Airplanes CEO —wrote the company's leadership team "has been doing all we can to find common ground with the union." However, after a third round of negotiations with a federal mediator, "the union did not seriously consider our proposals," and instead made "non-negotiable demands" that the company could not meet.

Because of this, Pope said, "further negotiations do not make sense at this point and our offer has been withdrawn."

The 33,000 members of the International Association of Machinists and Aerospace Workers walked off the job last month after the rank and file voted to reject a contract agreement hammered out days earlier.

S&P Global Estimates Boeing Will Have $10B Cash Outflow This Year

S&P Global warned the strike was "increasing financial risk for the company," and estimated Boeing will have a $10 billion cash outflow this year as a result. The agency put its ratings on Boeing's debt on "CreditWatch with negative implications." S&P explained that reflects "the increased likelihood of a downgrade if the strike persists toward the end of the year."

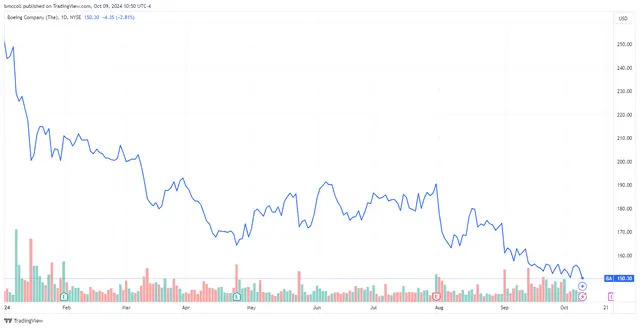

Boeing shares recently fell 2.2% to $151.26, trading near their lowest level in two years.

Read the original article on Investopedia .