News

Indonesia's Growing Nickel Production Disrupts Global Market

Via Metal Miner

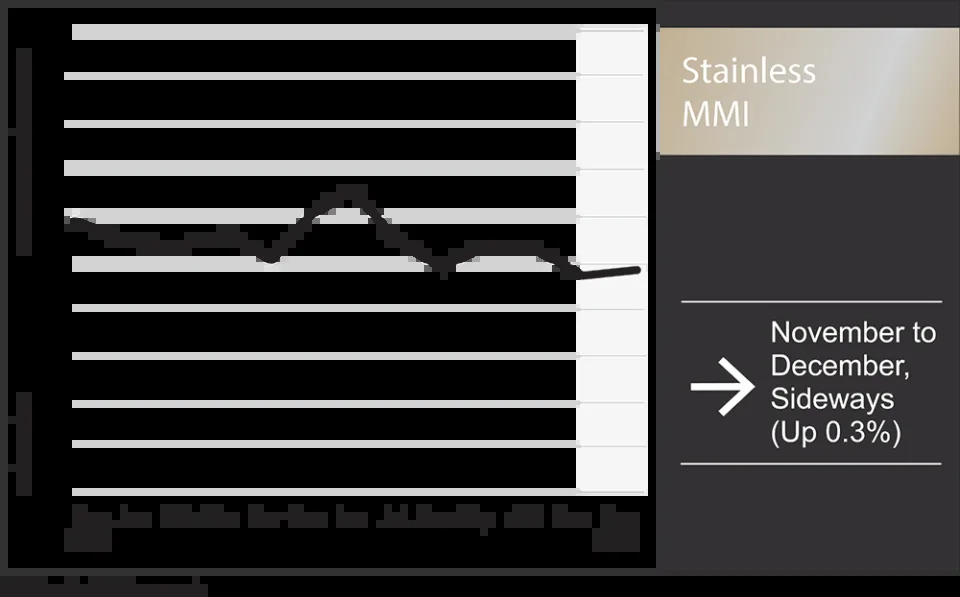

Overall, the Stainless Monthly Metals Index (MMI) steadied, with a modest 0.3% increase from November to December.

Stainless, Nickel Prices to Depart 2024 on a Low Note

Stainless distributors had nothing good to say about 2024 on the heels of the new year. To many, 2024 was mostly characterized by soft demand conditions and an oversupplied market. Mills largely managed to stabilize base prices and lead times. However, doing so required both capacity discipline and transactional discounts, which gave buyers increasing leverage in price negotiations.

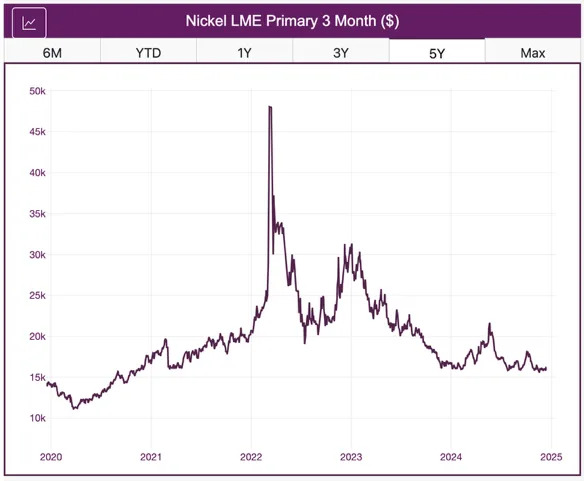

Meanwhile, Indonesia’s quest for dominance within the nickel market meant a substantial uptick in supply, especially amid EV demand challenges in the West. According to data from the USGS , Indonesia accounted for an estimated 48% and 50% of mine supply in 2022 and 2023, respectively. Throughout 2024, Indonesia’s share of the pie is anticipated to have grown even further, supported by rising production and the closure of mines elsewhere.

For the nickel market, all this added up to ballooning exchange inventories for both the LME and SHFE. However, this offered zero support to exchange prices, especially as Indonesia remains one of the world’s lowest-cost producers. As of December 12, LME inventories clocked a staggering 157% rise from the close of 2023, not much higher than the 152% increase in SHFE stocks.

Q1

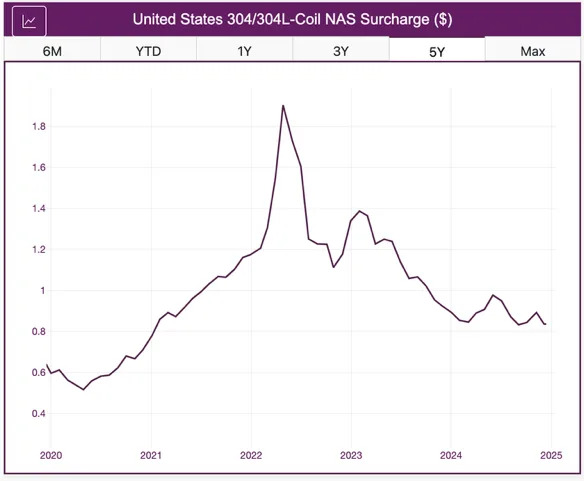

Following a nearly 46% year-over-year drop in nickel prices during 2023, NAS’ 304 surcharge opened 2024 at its lowest level since April 2021. Some stainless distributors noted a modest seasonal pickup in demand during the first quarter, but that proved mostly underwhelming relative to other years.

Buyers understandably showed no interest in buying ahead amid a falling surcharge and overstocked inventories. Meanwhile, mills worked to calibrate capacity to hold on to base prices, but this had no impact on the 304 surcharge, which fell by an additional 0.29% from the start of January to the beginning of April.

Q2

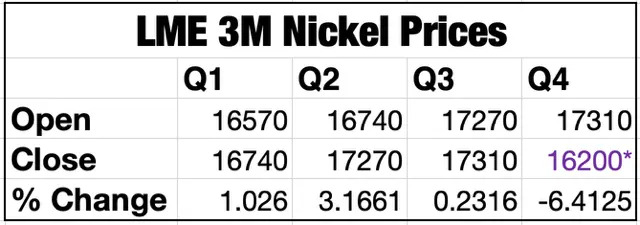

Toward the end of Q1, nickel began to perk up alongside other base metals, which helped lift nickel prices 1.03% higher from the start of 2024 to the close of March. This saw the NAS 304 surcharge find a bottom in April after more than a year of nearly uninterrupted declines.

While the fundamental narrative for the nickel market appeared largely unchanged, bullish sentiment among copper market investment funds had knock-on effects on nickel prices and overall liquidity. A sharp uptick in long positions saw market participation recover to its pre-2022 squeeze level.

However, the uptrend across the base metal category proved speculative. Nickel prices found a peak in late March, almost 29% higher than when they closed Q1. Still, this surge was followed by significant declines in the ensuing weeks.

The nickel price rise and subsequent retracement translated to a modest 3.17% quarter-over-quarter rise during Q2. Historically, stainless buyers tend to buy ahead when nickel prices rise. However, slow demand conditions saw no such increase. Major distributors Reliance and Ryerson witnessed a quarter-over-quarter decline in stainless steel shipments during Q2, weighed down by a well-stocked market. Read next: 5 Mistakes Buyers Can Make When Sourcing Stainless Steel

Q3

By the close of July, bearish nickel prices finally found a bottom. Albeit less than what was witnessed in Q2, the nickel market remained somewhat volatile in Q3, which translated to a fluctuating surcharge. Meanwhile, demand conditions remained largely unchanged, if not slower than what was witnessed earlier in the year.

While up year-over-year, both Ryerson and Reliance saw stainless shipments decline further from Q2. This occurred despite their offering aggressive discounts to mitigate the eroding value of their inventory.

Bearish conditions meant suppliers were uniquely hopeful that the early October port strike would cut off a substantial portion of the import market to help reduce the stainless supply glut that remains within the U.S. market. However, a protracted port strike did not come to fruition, so stainless remained a buyers’ market.

Overall, Q3 saw nickel prices rise by a modest 0.23%, while the NAS 304 surcharge fell 9.79% to open Q4 at its lowest level since the end of Q1.

Q4

By Q4, nickel prices stabilized, taking a pause from the volatility witnessed in previous quarters but continuing to show a downside bias. This also saw the NAS 304 surcharge steady, albeit at its lowest quarterly average for 2024. However, buyers showed no interest in forward purchasing. Still sitting atop well-stocked inventories amid lackluster demand conditions, many pushed off contracting, instead taking a wait-and-see approach to the market.

Overall, nickel prices fell 6.41% from the close of Q3 to where they stood as of December 12. Prices currently sit at their lowest range since April 2021, making nickel among worst-performing base metals of 2024, only a narrow second to lead. As we close the year, prices currently reflect a 2.23% decline since the close of 2023.

By Nichole Bastin

More Top Reads From Oilprice.com

Read this article on OilPrice.com